States given big role in implementing the act.

By Dr. Harpal S. Mangat

WASHINGTON, DC: There has been a lot of rhetoric about the Affordable Health Care Act with much misunderstanding on the current health system and how we compare to the rest of the world. The Affordable Health Care Act is designed to address the cost of healthcare and the lack of coverage by improving the quality of healthcare delivery.

In 2010, 84% of Americans had health coverage but the cost for both insured and uninsured was 17.9 % of the US GDP ($2.5 trillion).Other G8 countries spent between 9% (Japan) to 12% (Switzerland and Holland) of their GDP on healthcare. The difference between 17.9% and 12% for US is a trillion dollars.

Despite having the highest GDP expenditure on health care we rank 25 to 33rd in qualitative health outcome measures.For the decade prior to 2010 health care went up three times the rate of inflation manifesting in higher premiums, higher co-payments and higher deductibles.

Factors that drove up this cost included:

- The fact we pay for each and every procedure, medical device, or service not for the quality of healthcare.

- In most states there is no or little competition for health insurance. In forty of the states, 80 % of the market is controlled by one or two health insurances. Hence there is little competition, to limit prices and no incentive to cover pre-existing conditions.

- Paperwork cost for administering healthcare is not standardized and costs a dime on the dollar, more than Holland, the next highest spending nation.

- We pay an additional $70 billion dollars a year more on drugs than most wealthy countries.

- Americans have a higher incidence of preventable disease such as diabetes, and obesity related conditions that contribute to higher health costs.

The Affordable Health Care Act, as the name suggests, is designed to make it more affordable to obtain insurance for individuals/small businesses and to pay on qualitative outcome measures not on the number of procedures performed.States have been given a very big role in implementing the act, they are eligible for increased Medicaid funding for those who cannot afford and funds to set up market places for Individuals, families and small businesses to shop for value insurance policies.

Where are we with the law now

- More than 3 million under 26 have health coverage under their parent’s insurance.

- Six million seniors pay less for prescription drugs as Medicare closes the loopholes in Medicare part D program that caused the donut hole.

- One hundred and five million Americans have seen the lifetime limits on their health insurance abolished.

- Preventive care is less costly for 52 million Americans with no cost sharing.

- Seventeen million children cannot have health insurance denied for pre-existing conditions.

- Twelve million Americans have received rebates as health insurance companies have to spend eighty per cent of their premiums on healthcare(a major factor in slowing the rate of increase of premiums). Total savings on rates have been estimated at $2.9 billion to date.

- If a Medicare beneficiary is re-admitted within 30 days after discharge, the hospital has to cover the re-admission costs.

So far, the above measures have decreased the increase in health care spending over the last three years to 4%, the smallest increase in 50 years. Previously in the prior decade medical inflation was at three times the rate of national inflation.

What happens next

- As of January 2014 health insurance companies will not be able to charge higher rates for pre-existing conditions. Women cannot be charged higher rates than men.

- All American women will have maternity services for the first time as this becomes a mandatory requirement of every health plan.

- People with individual incomes of $15,860 and a family of four with a joint income of $32,500 will receive support for Medicaid payment to their state from the Federal Government and each state will adopted its own policy for that money.

- People with incomes of 138% of the poverty line ($15,860 for individuals & $32,500 for a family of four) to 400% of the poverty line ($45,971 for individuals & $94,202 for a family of four) will be eligible for a tax credit, the lower the income the higher the credit and vice-versa.

- Young persons at the age of 26 and above will be eligible for catastrophic coverage. However, these policies will not get tax credits.

- As of October 1st 2013 an anyone can logon to www.healthcare.gov or a state website to shop for the most appropriate policy. The tax credit will automatically be shown as a discount and the credit will automatically be sent by the government to the insurance company.

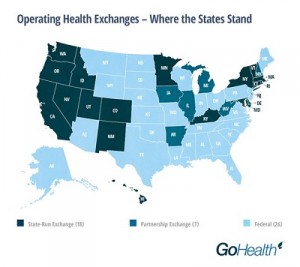

- To obtain this credit and buy health insurance all individuals or families will have to sign up on a designated site or call center between October 1st 2013 and March 31st 2014. The toll free national number is 1-800 318 2516 and the national website is www.healthcare.gov or go the state site e.g Maryland (www.marylandhbe.com), District of Columbia (www.hbx.dc.gov) , New York (www.healthbenefitexchange.ny.gov ) California (http://www.coveredca.com) those living in states that have not implemented state exchanges will be allowed to buy health insurance from the federal site see map below:

Buying Health Insurance for the individual and families will be like going to the Olympics with policies in bronze, silver, gold and platinum categories. The bronze will be the least inexpensive policy with the least coverage, platinum would be the most expensive with the most frills.

Buying Health Insurance for the individual and families will be like going to the Olympics with policies in bronze, silver, gold and platinum categories. The bronze will be the least inexpensive policy with the least coverage, platinum would be the most expensive with the most frills.- If a company employs 50 or more employees and do not give health insurance they will have to pay a penalty .However this will start in 2015.

- Small businesses will be able to buy health insurance for employees on their own market place called SHOP (Small business Health Options www.healthcare.gov/marketplace/shop) or alternatively they can keep their current insurance. There will be tax credits depending on total wages, for companies who participate in the market exchanges and buy health insurance.

- Under the new law there is a limit a health insurance can charge annually for premiums. For those at 400% of the poverty line (($45,971 for individuals & $94,202 for a family of four) the maximum will be 9.5% of their income. For those with 100-138% over the poverty line (($15,860 for individuals & $32,500 for a family of four) it will be 2%. Those in between will be on a sliding scale.

Harpal S. Mangat, MD, is in Practice in Maryland. He is an Assistant Professor at Howard University College of Medicine and on the Board of Maryland Collaborative Care, an Accountable Care Organization. He submitted recommendations to his US senator that got incorporated into the 2010 Affordable Health Care Act. He has two issued US patents and three additional patents that have been filed.

He is a graduate of the Royal College of Surgeons Ireland, trained at Trinity College Dublin, Oxford University and London University in Family Practice and Ophthalmology. In the US he trained at University of South Florida and Mercy Hospital Philadelphia in Ophthalmology and Internal Medicine. He is the transport physician for difficult cases returning to United Arab Emirates. His interests include innovative new technologies, Diabetes, Sleep Apnea and Lyme disease as well as long distance air transport of seriously ill patients.

He sees patients at his offices in Clarksburg www.clarksburgmed.com and Frederick www.mhcfred.com) Follow him on Twitter @DrHSMangat)